Even if your market has identified and reduced risks and has implemented risk management policies and procedures, accidents, injuries, and damage to property or claims can occur, for example:

- A customer trips, falls, and breaks their arm

- A canopy frame or sign blows away, hitting a customer or vehicle

- A car backs into a customer or vehicle

- Customers are ill, identifying food sold by a vendor as the cause

- A potential vendor challenges the board’s decision to deny their application

In most circumstances, these are resolved without a claim or legal conflict. However, when issues do escalate, costs and responsibilities can threaten a market and those responsible. The following content will help you understand how insurance is a way to transfer and share legal liabilities:

![]()

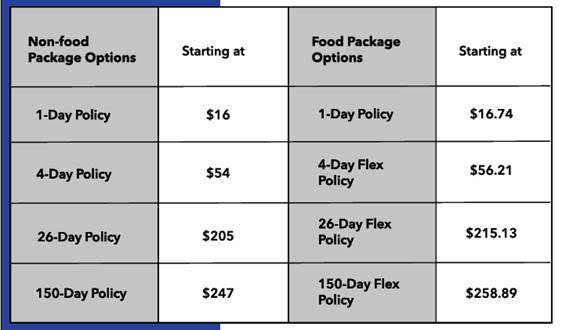

Due to the nature of the industry, Duuo Vendor Insurance policy prices are subject to increases without notice!

Pricing is based on a liability limit of $2 million and a booth size that is 200 sq ft or under. A food vendor is defined as someone who is preparing/serving food.

Please refer to Duuo’s Vendor Insurance policy summary for more details on what’s covered and their complete list of policy exclusions. (Food trucks excluded)

*FMO offers member markets annual Commercial General Liability (CGL) insurance for purchase, which covers most vendors while selling at their FMO insured member market. Vendors operating retail/wholesale outlets in addition to their market stand require their own CGL insurance. The insurance provided by Duuo is intended for individual vendors who are not covered by the FMO member market CGL insurance. Please confirm your market’s insurance requirements with your market manager.

- Identifying and Reducing Risk

- Managing Risk

- Transferring/Sharing Risk – Insurance

- Risk management forms and checklists